Education in purchase order financing (PO Finance) in crucial as very few lenders, finance brokers or operating companies know what the value proposition is.

PO Finance is not asset-based financing (factoring, debtor finance, equipment or mortgages) since the assets have not yet been created.

A purchase order is not an asset. It is simply a proposal for an interest to buy goods.

We hear the term “non-cancellable” – There is no such thing as a non-cancellable purchase order unless the terms are stipulated by a contract between buyer and seller.

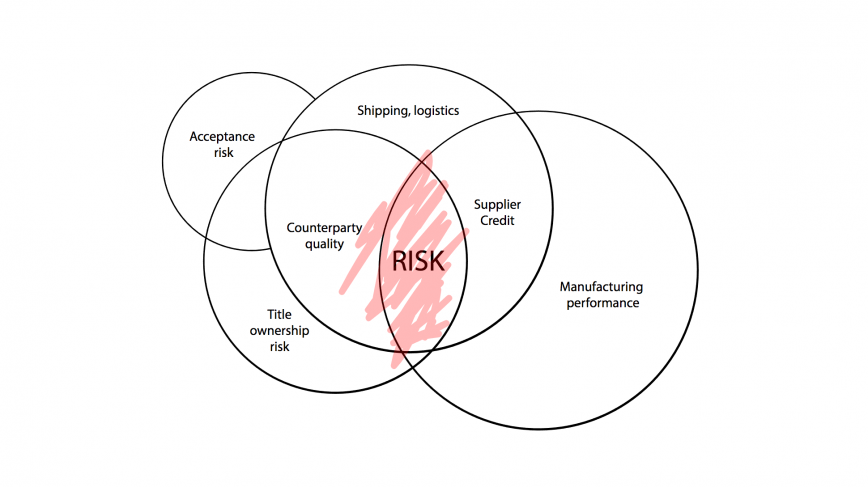

When PO financiers advance funds to a supplier for goods, they do so on a promise to pay (if the goods arrive, in working order, correct color, size, shape, deliver on time etc.). Performance of the transaction is highly risky given the complexities between counterparties. Asset-based lenders advance funds based on already established assets. Receivables, equipment, property etc are all prime examples that are assessed for capital raising.

Financing inventory to fulfill orders is an art, there is no set process due to the complexities of each buyer and seller supply chains such as;

- Deposits

- Mid-production payments

- Inspections, QC etc

- Shipping terms

- Payment Guarantees

- Border Jurisdictions

- Title ownership

- Customs clearances

- Duties, taxes, tariffs etc

- and more…

Financiers structure each client funding scenario based on the transaction/s presented. Funding is then injected along the supply chain to satisfy the procurement and delivery or goods right through to the end customer.

What makes PO finance particularly attractive is its “self-liquidating” attribute. When funding is provided to a supplier, funding is repaid commonly by the end customers receivable/s created from the sale. This creates the ideal cash flow position for the client as no repayments are required, providing zero impact to operational cash flow during the process of each drawdown of funds.

PO financiers help clients take advantage of growing sales by financing the purchase or manufacture of additional inventory to fulfill increasing sales without having to raise equity or pledge property assets.

Depending on the size or nature of the client’s transactions or trading position – Funding can include monitoring the inventory and deliveries to assure performance under the P/O requirements of timely delivery, quantity, and quality. This watchfulness offers assurances that safeguard both the lender and the client, maintaining a healthy funding relationship.

An example of a relationship between Stak and our referral channels in the factoring or trade financing world would be a situation where an existing client has established a big new customer relationship.

The client’s current sales are easily financed under a factoring arrangement; but, with the new relationship from a corporate retailer, they are going to need a lot of capital to pay for the inventory in order to procure the stock to deliver. This type of funding injects capital further up the chain before fundable assets are created.

The opportunity is great for the client’s business but they need a solution to help finance the increased inventory to fulfill the larger orders. The factoring (or other) lender wants to help but the orders are much larger than the asset base so they contact a purchase order finance company to discuss their new circumstances.

PO financiers like Stak assess the funding required based on the strength of the transaction rather than the balance sheet, trading history or even solvency.

Find out if Stak can provide funding for supplier payments

. . .

We regularly share our thoughts on trade finance, lending, company culture, product strategy, and design.

Stak works with clients that sell to some of the largest buyers in Australia & overseas.